Arthur Zucker

October 18, 2021

Reinforcement learning, lesson 1

Introduction

Basic RL model

In any RL model, there is :

- an RL agent

- an Environment, deterministic or stochastic

- actions

- rewards ( long/short term, intermediate)

- states (known/unknown)

- a goal: maximizing the reward function

1. Markov Decision Process

A RL problem is modelled using Markov Decision Processes.

The RL interactions

The classic RL interaction is as follows:

We have a discrete decision time $t$ (which would be for example seconds), and at each timestamp :

- The agent selects an action $a_t$, based on $s_t$ the current state of the system.

- The agent gets his reward $r_t$

- The Environment moves to a new state $s_{t+1}$

📝 Markov chains

Markov Chains are the building blocks of RL. A Markov Chain is a stochastic (which means that it includes randomness ) model describing a sequence of possible events in which the probability of each event depends only on the state attained in the previous event1. In order to create a model, we need to introduce mathematical definitions.

$$ \mathbb{P}\left(s_{t+1}=s \mid s_{t}, s_{t-1}, \ldots, s_{0}\right)=\mathbb{P}\left(s_{t+1}=s \mid s_{t}\right)$$

📝 Markov Decision Process (MDP)

A Markov Decision Process is a tool, to model decision making when outcomes can be random.

- $S$ the (finite) State space

- $A$ the (finite) Action space

- $p(s'|s,a)$ the transition probability, such that $\mathbb{P}\left(s_{t+1}=s' \mid s_{t}=s,a_t=a\right)$

- $r(s,a,s')$ is the reward of the transition from $s$ to $s'$ taking the action $a$. The reward can be stochastic, but we can express its distribution, $v$ for $s,a$ as $v(s,a)$. Thus the reward can be writtent as : $r(s,a) = \mathbb{E}_{R\sim v(s,a)}[R]$.

Assumptions

Markov assumptions : the current state $s$ and the action $a$ are a sufficient statistic for the next state $s'$. This means that “no other statistic that can be calculated from the same sample provides any additional information as to the value of the parameter”2. Our statistic provides as much information as possible.

Time assumption : discrete time, at each step, $t\leftarrow t+1$.

Reward assumption : the reward is uniquely defined by a transition from a state $s$, to $s'$ and an action $a$.

Stationary assumption : transition and reward don’t change with time. Otherwise, it’s non-stationary.

2. Policy

- Deterministic, given the same set of state $S$, the action $a\in A$ will be chosen

- Stochastic, a probability distribution over the actions determines $a$.

Then, it can also be :

- ( stochastic / deterministic ) History-dependant

- ( stochastic / deterministic ) Markov (relies on the previous state)

- Non-stationary, then $\pi = (d_0,d_1,…)$

- stationary, then $\pi = (d,d,…)$

At each round t, an agent following the policy $\pi$ selects the actions $a_t \sim d_t(s_t)$ .

Markov chain of a policy

The transition probability of a random process $(s_t)_{t \in \mathbb{N}}$ with regards to a stationary policy $\pi$ is the following :

$$ p^\pi (s'\mid s) = \mathbb{P}(s_{t+1}=s' \mid s_t = s, \pi) $$

Every actions in $A$ (even if it does not take the state from $s$ to $s'$) has to be taken into account. Thus we deduce that $$ p^\pi (s'\mid s) = \sum_{a\in A} \pi(s,a)p(s'\mid s,a) $$

3. Optimality Principle

How do we evaluate a policy ?

📝 State value function

The state value function allows us to determine the effectiveness of a policy. Various definitions can be used depending on the problem at hand. For the following definitions, let $\pi = (d_1, d_2, …,)$ be a deterministic policy.

$$ V^\pi(t,s) = \mathbb{E}\left[ \sum_{\tau = t}^{T-1} r(s_\tau,d_\tau(h_\tau)) + R(s_T) \mid s_t = s; \pi = (d_1, d_2, …,) \right ]$$

Here, where $R$ is a value function for the final state. Here we compute the expectation of the sum of the rewards obtained taking actions according to the policy, and receiving the corresponding rewards. We have to take into account the Expectation because the decision process can be stochastic, and thus the Expectation gives the equivalent of the mean rewards in a stochastic model.

$\qquad$📝 It is usually used when there is a deadline to meet.

$$ V^{\pi}\left(s\right)\ =\ \mathbb{E}\left[\sum_{t=0}^{\infty}\gamma^tr\left(s_t,d_t\left(h_t\right)\right)\ \mid s_{0\ }=s;\pi \right] $$

where $0\leq\gamma<1$ is the discount factor.

$\qquad$📝 We implement it when there is uncertainty about the deadline, or intrinsic definition of discount

$$V^{\pi}\left(s\right)\ =\ \mathbb{E}\left[\sum_{t=0}^{T_{\pi}}r\left(s_t,d_t\left(h_t\right)\right)\ \mid s_{0\ }=s;\pi\right]$$

$T_{\pi}$ : first random time when the termination state is achieved.

$\qquad$📝 Used when there is a specific goal condition

$$V^{\pi}\left(s\right)\ =\ \lim_{T\to\infty}\ \mathbb{E}\left[\frac{1}{T}\sum_{t=0}^{T-1}r\left(s_t,d_t\left(h_t\right)\right)\ \mid s_{0\ }=s;\pi\right]$$

$T_{\pi}$ : first random time when the termination state is achieved.

$\qquad$📝 Used when the system should be constantly controlled over tim

Optimization problem :

The value function under that policy is the optimal value function : $V^* = V^{\pi^*}$

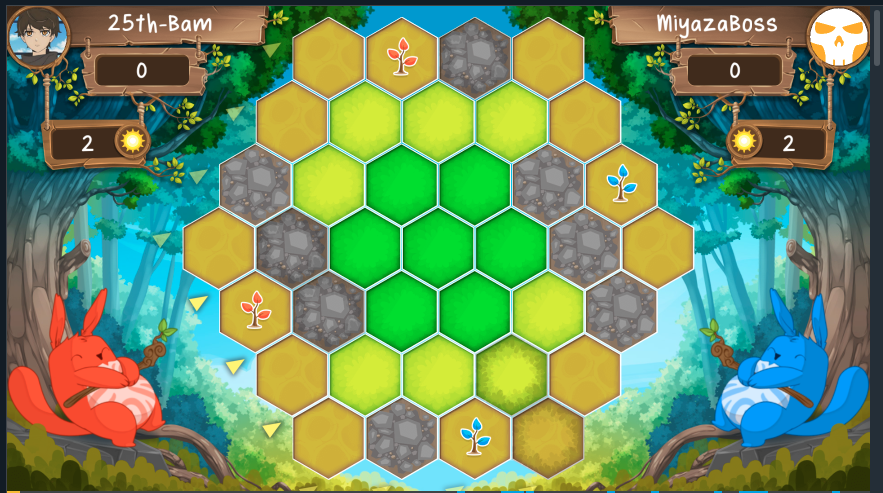

🎮 Application :

I will use a concrete and fun example of a game, where an RL agent can learn to win. The agent will play the 2021 Coding Game Spring Challenge, the Photosynthesis game (but a bit simplified)

Here, the environment is the board game. Let’s define the various notions that we introduced before in this framework.

- SEED : Planting a seed. It can only be done in the range of the size of the tree.

- GROW : Growing a tree. From a seed (size 0) to a sprout (size 1) to a sapling (size 2) to a mature tree (size 3)

- CUT : Cut a tree. Only mature trees can be cut

- WAIT : Do nothing

- Planting a seed costs

1 sun plusnumber of seeds already on the board-suns. (for example, in the figure above, planting a seed would cost 3 suns) - Growing a tree cost

size_of_the_tree-suns plusnumber of trees withe the same size on the board-suns. - Cutting a tree gives a

reward of3 suns . (let’s forget for now the quality of the soil) - Do nothing